CIH has just published a brand new edition of the book Housing in Northern Ireland, edited by Peter Shanks and David Mullins. Here CIH policy adviser John Perry, one of the authors, gives a flavour of what the new book offers.

Less than ten years ago there was a house-building boom in Northern Ireland. Completions of new homes rose from below 7,000 to a peak of almost 18,000 in 2006. The Republic of Ireland was booming too. While in that year there were 3.5 completions per 1,000 inhabitants in Great Britain, Northern Ireland had ten per 1,000 and the republic had 20. There was an Ireland-wide property boom and rapid growth in house prices, as well as a period of sustained household growth – almost 7,700 new households were created annually in Northern Ireland, on average, between 2001 and 2011.

But then came the credit crunch. New development fell back sharply, so that in the first five years of the current decade, output was down to an average nearer 5,000 per year. Household growth has fallen too, it’s now projected at under 4,500 per year up to 2022. However, unlike the rest of the UK house prices are struggling to recover and are still barely half of their 2007 peak.

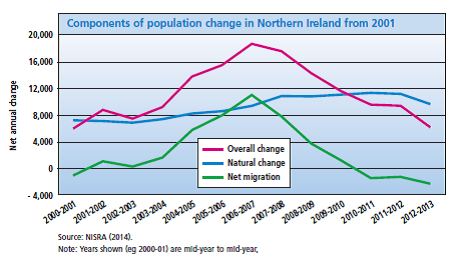

Changing housing demand reflects population trends that have been strongly influenced by migration. In the period between 2001-2011, a study for the Housing Executive concluded that there were “wildly changing patterns of migration and numerous changes in trends”. The net migration losses of the previous two decades were suddenly reversed, with a net migration gain of 38,000 by 2011. However, as the chart shows, trends fluctuated over the decade, with a sharp peak in net migration in 2006-2007 which then fell back so that currently there are again more people leaving Northern Ireland than there are arriving.

As in its economy and housing market, migration trends in Northern Ireland have mirrored those in the Republic of Ireland much more than those in the rest of the UK: the republic experienced a peak in migration at about the same time while the UK’s net migration has fluctuated over the last decade and still remains high. The official projection for Northern Ireland’s net migration is that it will stabilise at zero over the period to 2036, although such stability seems unlikely given recent experience.

It has fallen to social housing, now led by housing associations (HAs), to try to maintain output given the rapid decline in private sector new build, which is now producing only a little more than a quarter of the new homes it completed in the boom years. In the decade to 2010, HAs provided less than ten per cent of new build, but they have now increased their contribution to 21 per cent, with the private sector pulling back to complete only 4,700 units in 2015. Even so, new build by HAs barely exceeds 1,000 units per year, with around an additional 50 per cent of affordable units each year coming from acquisitions or conversions of existing stock.

What is signalled after the recent Northern Ireland Assembly elections? The different parties all set targets for new social and affordable housing, ranging from the DUP’s 1,600 units per year to a very ambitious 3,000 per year from the SDLP. In practice, output is likely to depend on three critical factors. First, after the compromises made in adopting only some of Whitehall’s welfare reforms, will the Assembly’s budget actually be able to sustain the investment required and, if it does, will HAs have the capacity to raise investment levels still further? Second, what will happen to the Housing Executive, whose existing stock faces a daunting repairs backlog, with decisions pending on its future as a landlord and how the investment it needs can be funded? And third, can the planning system be mobilised to deliver affordable housing as ‘planning gain’ from private development schemes, and is the weakened market now strong enough to be able to deliver it?

All of these questions and many more are dealt with in the new . It tells Northern Ireland’s unique housing story: shaped by the need to tackle very poor housing conditions in an environment of political conflict and sectarian violence, it has had historically high investment levels, Britain’s largest public housing authority, and a housing market influenced at least as much by the neighbouring republic than by the rest of the UK. While sharing many common policies with England, like its counterparts in Scotland and Wales the devolved government is now starting to carve out distinct housing policies. This book describes the trends that are beginning to emerge.

Original post: Chartered Institute of Housing

John Perry lives in Masaya, Nicaragua where he works on

John Perry lives in Masaya, Nicaragua where he works on